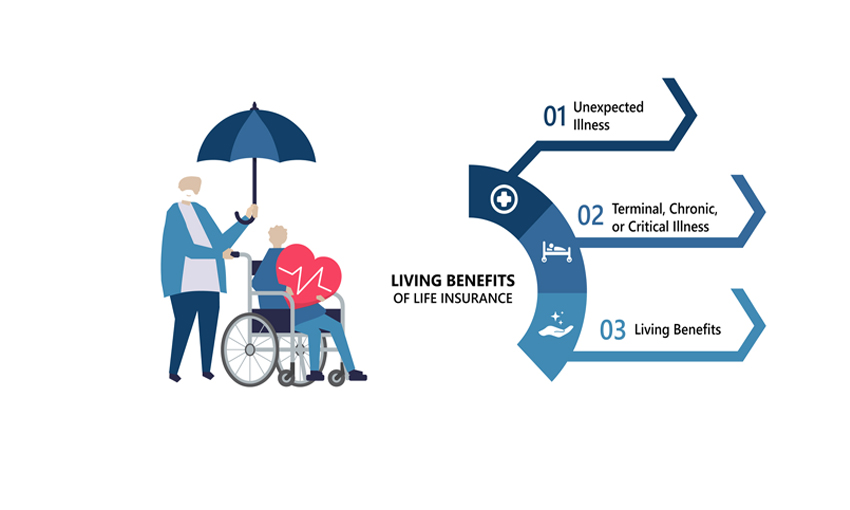

Living Benefits of Life Insurance

Most individuals take on a life insurance policy so that when they die their beneficiary may have financial security. Traditional life insurance policies do not, however, cover the costs when the insured has a critical, chronic or terminal illness.

Some term life insurance policies offer an add on referred to as “living benefits”. These add on can provide relief to the insured individual from the expensive cost of these illnesses.

In cases when a long-term, terminal or catastrophic illness befalls the insured individual he can have access to these benefits while he is still alive.

Dealing with an Unexpected Illness

According to the American Heart Association, cardiovascular disease accounts for 1.73 million deaths a year making it the leading cause of death worldwide. The number is expected to be over 23.6 million by 2030.

The American Cancer Society likewise says that there is an estimated 1.7 million new cancer cases diagnosed worldwide with half a million deaths coming from the U.S.

The U.S. Department of Health and Human Services says that long-term care in a nursing home for a semi-private room can be over $6,000 per month. Care in an assisted living facility on the other hand can exceed $3,000 per month.

Many people think that having a disability plan or health insurance is enough to cover the expenses of serious or sudden health problems including a stroke, heart attack or cancer. They are however not prepared for terminal, critical, or chronic illness.

While a health insurance plan may cover most of the medical expenses of such an illness, the patient first needs to deal with copayments, deductibles, and personal expenses.

A health plan will not be able to compensate for your lost income while you are sick or recovering from an illness. A disability plan, on the other hand may only be able to compensate for half of the wages you stand to lose.

There are two inevitable things that happen in cases of unexpected illness: your income will decrease and your expenses will increase, resulting in debt and financial paralysis. These situations may happen regardless of your age, income, and the type of health insurance you have.

Harvard researchers say that medical problems are the direct cause of over 60% of personal bankruptcies in the U.S. The sad part is 80% of those critically ill persons included in the study had health insurance.

This is to say other than a health insurance and disability plan there is a need for additional protection. A life insurance with living benefits or accelerated death benefit rider can be a big help at this time of financial crisis.

Dealing with a Terminal, Chronic, or Critical Illness

You developed a chronic illness and will need long-term treatment to get better, or perhaps you just had a stroke, heart attack or have just been diagnosed with cancer. Even if you have these medical conditions you can still get your life back provided you have the funds for proper care and treatment.

John Seffrin, CEO of the American Cancer Society says that there are still an increasing number of people who cannot afford proper care and treatment for serious medical conditions. He further says that because of financial constraints, many people choose to turn down treatment.

A report from USA Today says that one-fourth of cancer patients and their families have depleted their savings to cover the cost of treatment. Additionally, one-eighth of those with advanced stages of cancer have completely turned down recommended proper care because of high costs. While you may have health insurance coverage, sadly it will only cover a small portion of the costs.

Would it not be extremely helpful if instead of depleting your savings account you can have access to your death benefit? This can be a big help in paying for the cost related to proper care of your serious medical condition.

If you qualify as being terminally ill, some insurance companies can accelerate most of your death benefit but it just does not sound too good. A life insurance policy with added living benefits is a better option because you are covered in these areas:

Terminal Illness

If you have been diagnosed with a terminal illness with a life expectancy of 12 to 24 months, you will typically receive a benefit. You can use these funds to prepare for final expenses, any experimental medicines you may have heard of, or on anything you deem worth spending on.

Chronic Illness

If you have chronic illness and are not self-sufficient in dressing up, bathing, or eating, you will typically receive a monthly benefit. This could run up to about one-fourth of your death benefit amount annually.

Critical Illness

Typically gives you a lump sum amount if you have a serious illness which may include a stroke, heart attack, or cancer.

There may be some restrictions when you avail of the living benefit attached to your life insurance policy. You can discuss with a licensed Aha Life Insurance agent (1-866-816-2100) details concerning the added living benefits option to your life insurance coverage.

Life Insurance with Living Benefits

A life insurance with living benefits gives you the option to receive a portion of your death benefit to cover costs in relation to your illness. You can qualify for this benefit if you a terminal, chronic, or critical illness which may include stroke, cancer, or heart attack.

Any amount paid to you for this purpose will be deducted from the death benefit your beneficiary will receive when you pass. Despite that provision, being able to accelerate a portion of your death funds could mean a huge help to you and your family in dealing with your health crisis. It may even be the reason to enjoy a healthier and longer life.

Call a licensed Aha Life Insurance agent at 1-866-816-2100 and ask how your traditional life insurance coverage can be added with living benefits.